Global Ad Spend +5% in 2014 and 2015

September 11, 2014

![]() Carat published its updated forecasts for worldwide advertising expenditure in 2014 and 2015, with market optimism demonstrated through strong global and regional forecasts.

Carat published its updated forecasts for worldwide advertising expenditure in 2014 and 2015, with market optimism demonstrated through strong global and regional forecasts.

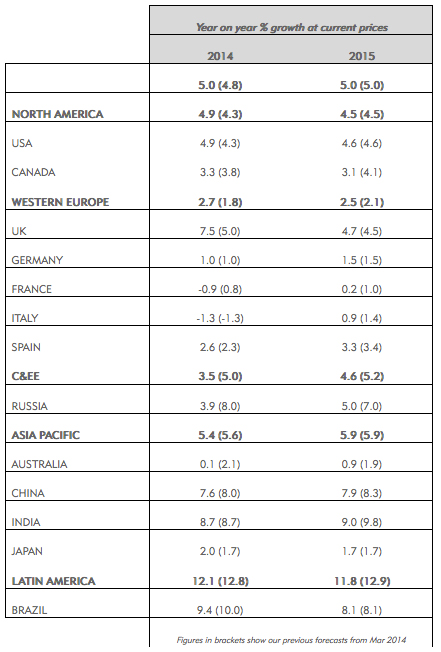

Based on data received from 59 markets across the Americas, Asia Pacific and EMEA, Carat’s latest forecast show overall global advertising revenues accelerating by +5.0% in 2014, an increase on the +4.8% predicted in March 2014, and reaffirming positivity for 2015 with year-on-year growth predicted at +5.0%.

From a regional perspective, Carat predicts further positive momentum in 2014 for North America and Western Europe, compared with figures announced in March 2014. The US continues to show strong on-going market growth, with levels of advertising spend in North America expected to exceed the pre-recession peak in 2007 for the first time by the end of 2014. Western Europe is predicted to see a return to positive growth of +2.7% after two consecutive years of declining advertising spend, driven by a strong UK advertising market forecast to grow by a robust +7.5% this year.

Whilst forecasts show a slight decline in growth when compared with predictions from March 2014, Asia Pacific and Latin America are still both forecast to outperform global predictions, with growth rates for 2014 of +5.4% and 12.1% respectively, and the only regions to see double digit growth in some markets. Carat’s data also highlights that the outlook for 2015 continues to be encouraging with all key markets forecast to return to positive growth.

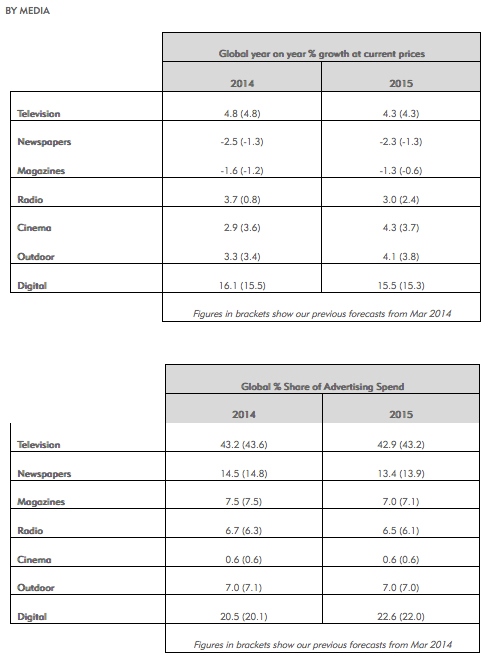

By media, Digital outperforms previous predictions for 2014 with year-on-year growth forecast at +16.1%. Digital will also increase its total share of spend, reaching 20.5% in 2014 and 22.6% next year, when it will outpace the combined Magazines and Newspaper global share for the first time. Whilst the steady decline in Print* is expected to continue, all other mediums are predicted to achieve year-on-year growths of approximately 3%-5% in 2014 and 2015.

Figures in brackets show our previous forecasts from Mar 2014

Commenting on the Carat Advertising Expenditure forecasts, Jerry Buhlmann, CEO of Dentsu Aegis Network, said:

“Carat’s latest advertising forecast gives us increased optimism for the outlook of global and regional advertising spend. With the global recession further behind us and a healthy trend of 5 per cent year-on-year global ad growth, there is positive momentum building across the industry.

“Whilst Digital continues to headline market trend discussions, the components within this dominant media now provide the interesting chapters, with the opportunities in mobile leading the debate. With changes and trends in consumer behaviour driving business opportunities, brands need to deliver innovative and integrated solutions to reap the rewards ahead.”

REGIONAL BREAKDOWN

NORTH AMERICA

There is continued optimism for a solid year in the US advertising market, with +4.9% growth predicted for 2014 thanks to the on-going economic recovery and new technological advances in all media. Confidence in the US advertising market is expected to continue into 2015, with a +4.6% year-on-year increase thanks to a continually improving economic landscape.

• Digital spend will grow faster than all other media, up +16%, with the biggest drivers being Mobile at +37% year-on-year growth and Online Video at +40%.

• TV is expected to increase at +3% this year; Out-of-Home (OOH) and Cinema will increase by +2.6% and +3.1% respectively.

• Both Newspapers and Magazines, with rates of -0.5% and +0.5% respectively, are focused on increasing programmatic buying to try to stop the flow of dollars to Digital.

• Radio is predicted to see a +3% increase in 2014 mainly due to political campaigns and the implementation of the Affordable Care Act.

Carat forecasts moderate growth in Canada for both 2014 and 2015 (+3.3% and +3.1% respectively).

• Demand for TV remains stable at +1.5% this year, and while broadcast partners for the Winter Olympics and FIFA World Cup saw robust markets, these did not represent significant new revenue into the market and non-sporting event broadcasters are reporting a somewhat soft advertising market.

• Consistently high double digit growth rates for Digital media are predicted, which will see it overtake TV to become the biggest media type by 2015, with a 35% share of advertising spend. This growth is fuelled by year-on-year growth of +15.1% for Paid Search, +55.9% for Mobile and +12.3% for Online Video.

• Out-of-Home continues to perform well, at +5.3%, as investment in digital screens has almost doubled in the past three years.

• Radio remains the last true local broadcast medium, and the most effective for local businesses, and revenues anticipated to increase by +1.7% in 2014.

WESTERN EUROPE

In Western Europe, after two years of decline the outlook is back to positive growth with of +2.7% predicted this year, and +2.5% in 2015. Growth in the region is driven by a strong UK advertising market which is expected to grow by +7.5% this year, and a cautious but improving market in Germany but also by markets such as Spain, Greece, Ireland and Portugal, which are all forecast to return to positive growth in 2014 after many years of declining year-on-year advertising spending.

The UK advertising market is having a very buoyant year boosted by the FIFA World Cup, improving economy and double digit growth in Digital media spend. As a result, the 2014 forecast for advertising revenue has been revised upwards significantly, from +5.0% year-on-year growth in the March 2014 report to +7.5%. Growth in the UK market as a whole is expected to continue into 2015 with a +4.7% year-on-year increase.

• Digital media in the UK is predicted to grow by +17.5% in 2014, accounting for over 42% of total spend. Paid Search, which has a 53% share of total digital spend, is forecast to grow year-on-year by +11.4% in 2014 and Display spend (which includes Online Video, Mobile and Social Media) which accounts for 34% of total digital spend, is predicted to grow by 33% in 2014.

• Forecasted revenue for TV has now risen to +7.5% for full year 2014, on the back of strong H1 figures, surpassing previous estimates, driven by strong ad spend on ITV1 and Sky.

• The FIFA World Cup, arguably the biggest event of the year, saw June revenue up by +4.6%, the majority of which was driven by ITV1, which was up +24.7% in the month.

• OOH performance for H1 2014 was up 2% and Cinema growth is bolstered by the fact that it is 100% digital now, which opens up the medium to new clients that need flexibility and short turnaround times.

• Overall Print continues its slow, steady decline although, bucking the trend is the Free Sheet market, which continues to flourish.

• By category, the leading category Retail increased advertising spend in the first half of 2014 compared with the same period in 2013 by +15.6%, Financial Services and Insurance increased by +6%, Automotive by +16.7% and Telecommunications by +21.4%.

In Germany, there is greater optimism in 2014 than in 2013, however the year-on-year forecast stays a cautious +1.0%. In 2015, Carat expects to see further growth, thanks to a predicted improving economic outlook and subsequent greater confidence of advertisers in consumer spending habits.

• Digital media spend again continues to show the highest rate of growth of all media channels at +14.4%.

• Television, Radio and Outdoor advertising spend will increase moderately.

• Newspapers still struggle with a decline of -6.6%. Print publishers are investing strongly in digital platforms, offering their titles via several touch points. Magazines buck the trend a little with a smaller year-on-year decrease of -1.0% in 2014.

• Despite the improved attractiveness of Cinema, thanks to the near complete digitalisation of cinema screens, advertising spend are still expected to recover only slowly with a still significant decline of -6.7%.

• Nearly all the top 10 categories are expected to show positive growth in gross advertising spend in 2014, with Finance and Beverages being the only exceptions, with a predicted contraction of -3% and -5% respectively.

Advertising expenditures in France are predicted to decline marginally year-on-year by -0.9% in 2014, due to continued economic uncertainty and a disappointing H1 performance. However, the full year forecast for 2015 is encouraging, with a return to positive figures expected (+0.2%), following three consecutive years of declining advertising spend.

• Digital media is forecast to buck the overall market trend with growth of +3.6%. Paid search remains the principal investment vehicle, with a 70% share of the digital market in 2014. PPC will grow by +4.2% driven in part by an increase of search requests on mobile and tablet. Display spending may see a slight year-on-year decrease of -1.1% as advertisers embrace programmatic buying.

• Although the Winter Olympics and FIFA World Cup provided a positive boost for broadcasters and new DTT channels that have also proved attractive to advertisers, overall TV advertising spend is still expected to continue to decline by -0.5%, albeit at a slower rate than in the previous two years.

• Newspapers are down -5.2% and Magazines -8% but both still continue to receive a significant proportion (23%) of total media spend.

• After two years of decline, Radio advertising expenditures are expected to grow this year by +1% and Cinema is forecast growth +3% in 2014.

The advertising market in Italy is forecast to decline by -1.3% in 2014 – still a contraction but much less than in previous years (-10.3% in 2013 and -11.9% in 2012). The market is moving in the right direction, with positive growth forecast to return in 2015 (+0.9%).

• Only TV and Digital are expected to grow; other media types are forecast to decline in advertising spend.

• Television, the medium most affected by the major sporting events this year, is showing signs of recovery with growth this year of +1.4% after year-on-year declines since 2011. The growth is driven mostly by the digital channels and Satellite, which means that TV is able to maintain its dominance in the overall market (53.4% share).

• Digital media has the second largest share of advertising spend in Italy (21.2%) and is showing the highest growth rates at +7.4%. Double digit increases are also expected for Mobile at +23.6% and Video at +25%.

• In contrast, Print, OOH and Cinema are showing contractions of greater than 10%; although Radio is holding up better with a smaller decrease of -1.1% vs. 2013.

It is back to positive figures for the advertising market in Spain in 2014 with forecast growth of +2.6% for 2014. The 2014 trend is expected to continue into 2015, with an increased growth rate of +3.3%.

• All media types are forecast to return to growth in 2014 with the exception of Print, which still continues to suffer advertising revenue declines due to falling readership and circulation (Newspapers down -5.1% and Magazines down -4.7%). Online versions perform well in terms of audience and consumer demand but do not yet receive enough monetization.

• Share of Digital media spend (22.4%) will exceed the combined share of Newspapers and Magazines (21.1%) for the first time in 2014. Overall Digital spend is forecast to grow by +6.7%, driven by Search at +7.8% and Mobile +24% growth.

• TV remains the destination for the lion’s share of advertising spend (42.2%) with consumption remaining high. TV advertising spend is forecast to grow by +4.7% in 2014 and +5.3% in 2015. OOH will also see moderate growth of +2.2%, revitalised by new formats and digital signage.

• A significant increase of +15% is predicted for Cinema this year, with strategies such as digitalisation and alternative theatre income (e.g. the broadcasting of sports events), coming to fruition.

• Retail is the leading category, with a +10.2% forecast growth in gross advertising spend in 2014.

CENTRAL AND EASTERN EUROPE

Growth in the Central and Eastern European region has been revised down to +3.5% from +5.0% previously forecast in March 2014, reflecting the continued political and economic uncertainty in the region. Downward growth revisions are being led by Russia.

Predictions for the Russian advertising market have been revised down from +8.0% to +3.9% due to the continued uncertainty of the economic and political situation. The advertising market was however boosted in the first half of the year thanks to the Sochi Winter Olympic Games in February but more moderate growth is forecast for the rest of 2014. In 2015, growth in the Russian market is forecast to continue at a rate of 4.0-5.0%.

• Despite Digital’s high growth rates, TV still commands by far the highest share of total media spends: 47.9% in 2014. The Sochi Olympic Games were a key driver for TV ad spending in Q1 2014. Overall TV ad spend is forecast to grow by 4.0-5.0% by the end of the year (10% for regional TV and 3% for national TV.)

• Digital is the second most popular medium in Russia, with 24.1% share, and continues to be the fastest growing medium with +14.7% growth in 2014, driven by paid search up +20.4%.

• With declining circulation, Print advertising revenue is forecast to drop -10% this year.

• Due to continuous legislative restrictions, OOH revenues are forecast to decline in 2014 by -5%, whilst Radio is forecast to increase at a moderate pace of +5%, with Retail and Automotive being key drivers of Radio advertising spend.

ASIA PACIFIC

In the Asia Pacific region, growth has been revised down marginally in 2014 from +5.6% to +5.4% as the economy in top spending market China stabilises and market conditions in Australia still recover. The outlook is positive however for Japanese advertising spend and there is buoyancy in the Indian advertising market boosted by the elections. Double digit increases continue in markets such as Indonesia and Vietnam. The outlook for the region in 2015 is a healthy +5.9%.

Stable growth of +7.6% is forecast in China – although this has been revised downwards due to the reduced spend in Real Estate, Alcohol and Food. With the economy stabilising after many years of fast-paced expansion, the advertising market is predicted to maintain a solid growth rate of +7.9% in 2015.

• The beverage sector is the largest category in China, but revenues are expected to shrink by -1.3% this year. The food category is forecast to contract by -3%, while Real Estate will drop outside of the top 10 for the first time.

• Digital media spend in China continues to grow at a pace – up +33% in 2014 and +30% in 2015; significantly higher than any other media type. Growth is driven by mobile and programmatic buying.

• TV still has the highest share of spend, at 57% of the total. TV is forecast to have a moderate increase in 2014 (+5.4%) and 2015 (+5.0%).

• OOH, the third most popular medium in China is forecast to grow +5.7%, driven by airport, metro and digital OOH spends. However, with moderate economic growth advertisers are tending to be more conservative, with most investments concentrated in the higher tier cities.

• As in other markets, newspaper and magazine readership in China is in decline. Both national and local/regional titles are losing readers, with more and more people turning to digital platforms for news such as their mobile apps. Newspapers are forecast to decrease by -8.7% and Magazines by -7.7% this year.

• Radio is enjoying solid growth (+8.0%), due to the ad spending growth in the Automotive industry.

In Japan, advertising expenditures for 2014 have been revised up from the +1.7% growth predicted in March 2014 to +2.0%, due to the improving Japanese economy improving Japanese economy achieved by ‘Abenomics’ prime minister Shinzo Abe’s package of economic policies. The trend of growth in advertising spend is forecast to continue with an increase of +1.7% in 2015.

• Advertising spending is expected to increase across all media this year, with the highest growth rate expected for Digital media at +7.0%.

• Television, which has the largest share of the market, is forecast to enjoy stable growth with an increase of +2.2%.

• The expected growth rates for Newspapers and Magazines are +1.1% and +0.4% respectively.

• The outdoor advertising market (outdoor ads and transit ads) is predicted to grow by +2.1% year-on-year. Digital OOH is expected to continue growing, with the Outdoor market predicted to increase +1.7% in 2015.

• Radio advertising spend is forecast to be up +1% in 2014 and +0.6% in 2015.

In Australia, total advertising expenditures are predicted to hold steady this year at +0.1%. The present economic conditions point to a cooling of consumption as consumers seek to reign in their debt in a general environment of uncertainty that has been exacerbated by belt tightening of the new government. The Winter Olympics, FIFA World Cup, recent Commonwealth Games and upcoming Victorian state elections in November have not and are not forecast to have a significant effect on advertising expenditure. The market is predicted to be moving in the right direction in 2015, with a rise in growth forecast at +0.9%.

• Digital media and Outdoor spends are expected to grow in 2014 by +16% and +4.3% respectively, with Radio holding steady at +0.3%. All other media showing a decrease in advertising spend.

• Free to air Television is starting to show signs of losing revenue to Online Video channels, although broadcasters collect a proportion of this via their own catch-up TV sites. Both FreeTV and PayTV experienced declines in revenue in the first half of 2014 (-1.5% and -9.8% respectively). Total TV is forecast to decline by -2.6% in 2014.

• As in other markets, Print media has been losing circulation, readership and subsequently revenue, with double digit advertising spend losses expected (Newspapers -15% and Magazines -14%).

• Growth is expected to be led by Automotive (+2.5%), Banking and Finance (+8.8%) and Insurance (+7.2%). Whilst consumers demonstrate a desire to save in more basic areas, they continue to spend on Cars and Travel – partly driven by a more cash-rich, ageing population.

The elections in Q2 2014 in India have driven buoyancy in the market and there is an upswing in the mood of the country. Overall advertising spend is predicted to see a spike in 2014 driven by huge spends by the political parties. The advertising market is to see a +8.7% year-on-year growth in 2014. Growth is to continue into 2015 at +9.0% as advertisers embrace new technologies within Digital. The Cricket World Cup is also predicted to bring about higher investments from advertisers.

• Print media was the biggest beneficiary of the political party spends, and unlike other markets, Newspaper spend will grow by +6% in 2014. Newspapers are still the most popular media type in India with 37% share of total media spending.

• Digital media spend in India is the third most popular media type behind Newspapers and TV, and it is forecast to grow by +33.2% this year with growth driven by Mobile and programmatic trading. Advertisers are increasingly thinking ‘mobile first.’

• Mobile internet access is almost equal to desktop internet usage in India, and the importance of mobile in the coming years will grow. With the upcoming launch of 4G services across India later this year, the opportunity for advertisers is huge.

LATIN AMERICA

The LATAM region continues to achieve the highest advertising growth rates with a +12.1% growth forecast in 2014 driven by highest spending market Brazil, but also double digit growth in Argentina (lifted by high inflation in the market) and Colombia, at +31.3% and +13.2% respectively. The LATAM region is forecast to grow by +11.8% in 2015.

In Brazil advertising expenditures are forecast to increase significantly by +9.4% in 2014 boosted by the FIFA World Cup and general elections.

• Year-on-year gains in advertising spend are forecast across all media types.

• Amongst the top 10 categories, the Retail sector remains the top spender with growth of +2% in H1 2014 compared to the same period in 2013. During this period Cosmetics and Personal Care the second highest spending category increased spends strongly by +13%. The highest growth rate however was posted by the Food sector, at +55%. The only key sector to see a year on year decline in advertising spend in H1 2014 was Automotives at -1%.

• Good advertising expenditure growth rates are forecast to continue in 2015, with a predicted growth rate of +8.1%.

Figures in brackets show our previous forecasts from Mar 2014

Broken down by media, Television continues to command the highest share of advertising spend globally +43.2% this year. It has benefited the most from the sporting events – Sochi Winter Olympics and FIFA World Cup this year with a peak in year-on-year growth rates of +4.8%. Outdoor advertising revenue growth has been driven by growth in digital OOH spend. It has seen a relatively strong year of growth this year at +3.3%, with share of spend holding steady at 7%. Radio continues to see stable moderate growth of +3.7% this year with demand for its competitive costs and flexibility ensuring it maintains its share of the advertising pie. Radio advertising spends are forecast to increase by +3.0% in 2015. The digitalisation of Cinema has increased the flexibility and turnaround times for the medium. Growth is expected to be particularly strong in 2015 with a predicted +4.3%, supported by a strong film release schedule.

Globally Digital media spending overtook Newspapers in 2012, but still newspapers command the third highest share of spend at 14.5%. Newspapers are however seeing a decrease in share by on average 1% point year-on-year, with Newspaper share of spend predicted to fall to 13.5% in 2015. Year-on-year steady declines in Newspaper advertising spending continues with a predicted -2.5% in 2014 and -2.3% in 2015. It is a similar story for Magazines, although year-on-year declines in ad spend have been less severe, -1.6% in 2014 and -1.3% in 2015. Share of Magazine advertising spend is falling by on average half a percentage point year- on-year with share at 7.5% in 2014 contracting to 7.0% in 2015. Print publishers continue to invest strongly in digital platforms, offering their titles via several touch points, however so far digital revenues have not be able to make up for lost traditional print revenues.

It is Digital media spend however which has been increasing in leaps and bounds. Its share of spend at 22.6% in 2015 is forecast to overtake Newspaper and Magazines combined share of spend (20.4%). Digital’s share of total spend has been increasing by on average 2% points each year with double digit growth rates year after year, the forecast is +16.1% for 2014 and +15.5% in 2015. Growth is driven by Mobile, Online Video and Social Media.

Mobile (including tablet) advertising was slow to take off, but has now become a very significant part of digital advertising spend, largely driven by Google and Facebook, who collectively account for an estimated 70% of all global mobile ad spend. Mobile has grown reflecting the greater amount of time people are spending on mobile devices, as mobiles have become more essential to people’s lives.

Faster connection speeds have helped video to become a hugely important part of people’s online behaviour. The rise of video has seen video ads become more accepted online, and now most YouTube videos are accompanied by advertising, with 75% of the in-stream ads now skippable. Facebook is also actively selling video ads, and has recently allowed them to play automatically on desktop and mobile. As other publishers like Buzzfeed and Vice get more actively into video Carat expects this to continue to grow quickly.

Advertising remains the way that social networks are funded, at least in the West. Facebook now makes the majority of its ad revenue from mobile ads, particularly the ‘app install’ ads, which Twitter has also introduced. Ads have also come to Instagram, and given the amount of time that is spent on social, Carat expects this to continue to rise.