Connecting what Consumers demand with what Shoppers Buy

December 19, 2013

![]() When consumers head out for their everyday shopping needs, are they navigating the store on auto-pilot or are they open to new products and experiences? As with many of the puzzles marketers face, the answer here is anything but clear-cut. And in looking at the consumer engagement data behind 50,000 purchases across 100 fast-moving consumer goods (FMCG) categories in the U.S., the behavior here is quite varied. Nielsen’s recently published Category Shopping Fundamentals study provides good news for marketers in that there are ways to engage with shoppers, motivate them to shut off the cruise control and inspire more involved purchase decisions.

When consumers head out for their everyday shopping needs, are they navigating the store on auto-pilot or are they open to new products and experiences? As with many of the puzzles marketers face, the answer here is anything but clear-cut. And in looking at the consumer engagement data behind 50,000 purchases across 100 fast-moving consumer goods (FMCG) categories in the U.S., the behavior here is quite varied. Nielsen’s recently published Category Shopping Fundamentals study provides good news for marketers in that there are ways to engage with shoppers, motivate them to shut off the cruise control and inspire more involved purchase decisions.

Navigating Landscape Challenges and the Path to Purchase

Understanding the shopper’s path to purchase is vital for any marketer to unlock category sales opportunities. But today’s shopping landscape is growing more complicated by the minute, which heightens the challenge when it comes to reaching and connecting with customers. Shoppers are faced with fast-changing shopping environments, new store formats, in-store services, mobile marketing and innovative loyalty programs. Understanding across the shopper’s path to purchase is crucial in creating a roadmap that funnels traffic in your direction.

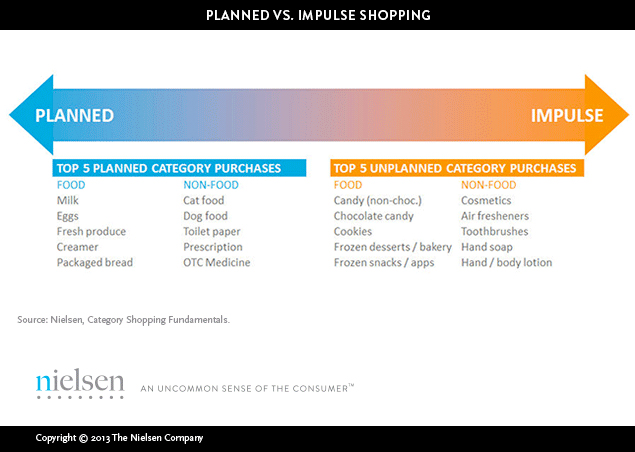

Consumers plan to buy 72 percent of the category purchases that end up in their carts before they even head to the store. To what extent a purchase is planned can help marketers weigh the importance of influencing these category shoppers on a pre-store basis to ensure they land on the so-called “shopping list.” Alternatively, the remaining 28 percent of purchases reflect reminder categories that may not be “top-of-mind” and the highly sought impulse buys.

Part of the pre-planned purchase behavior may be due to the fact that on average, nearly half of shoppers in the recent Nielsen study said they aren’t engaged in stores as they shop a particular category. So if consumers aren’t engaged, they’re essentially navigating the store on auto-pilot and making habitual purchasing decisions. Purchase-intent decisions, however, vary by category type. For example, the decision to buy a given food category is made in the store on 31 percent of instances, compared with 23 percent for non-food categories.

Part of the pre-planned purchase behavior may be due to the fact that on average, nearly half of shoppers in the recent Nielsen study said they aren’t engaged in stores as they shop a particular category. So if consumers aren’t engaged, they’re essentially navigating the store on auto-pilot and making habitual purchasing decisions. Purchase-intent decisions, however, vary by category type. For example, the decision to buy a given food category is made in the store on 31 percent of instances, compared with 23 percent for non-food categories.

Early engagement has become essential for marketers as U.S. shoppers claim to begin their planning with a brand in mind well ahead of their actual trips to the store. Product type, quantity and price are also on the mind of shoppers, but they play a more critical role while shoppers navigate the shelf. Due to this strong role of brands in the planning process, marketers must focus on engaging shoppers before they enter the store to convert planned purchases at the shelf.

Categories that Drive Trips and Engage Consumers

From a category perspective, nothing has more power to drive consumers to the store than milk (59% of instances), closely followed by pet food (56%) and baby food (52%).

A growing variety of channels is challenging the traditional grocery store format for many of these one-off category trip drivers. Small-format retailers compete with stores in more convenient locations, while larger-format mass merchandisers and club stores attract shoppers with everyday low prices and value. A better understanding of trip driving categories combined with channel preferences provides for collaboration opportunities between brands and retailers to better attract these shopping trips.

file

Possibly surprising, U.S. consumers appear to be engaged with only 48 percent of their purchase decisions. Said another way, consumers are making habitual purchases almost half of the time rather than engaging with products and making evaluative choices. And some of the least-engaged purchases involve common everyday products—some of which are among the biggest shopping needs, such as milk.

In fact, consumers report being the least engaged when they’re shopping for milk (29%), compared with a high level of engagement for indulgent purchases like frozen desserts (64%) and infrequent purchases like toothbrushes (64%). When evaluating strategies to boost engagement in the aisles, retailers will have greater success if they focus their in-store marketing efforts on departments where consumers have the freedom to choose and are engaged at the shelf, particularly the frozen and snack aisles.

When evaluating strategies to boost engagement in the aisles, retailers will have greater success if they focus their in-store marketing efforts on departments where consumers have the freedom to choose and are engaged at the shelf, particularly the frozen and snack aisles.

So when it comes to capturing the consumers’ attention for these categories, retailers need to market accordingly. For categories that shoppers typically buy while navigating the stores on auto-pilot, the key is to foster brand loyalty and leverage pre-store influencers like store flyers or coupons. In situations where a category draws a high level of engagement, retailers and brands have a great opportunity to influence purchases at the shelf. The growing use of mobile devices while shopping provides a new way to influence shoppers in addition to the more traditional sales promotions, merchandising displays and eye-catching packaging. In-store influencers can be particularly effective for smaller, niche brands seeking to capture unplanned, impulse purchases.

Execute a Winning Strategy

With the landscape the way it is, a marketer’s playbook can’t be the same across all categories. Less than one-fourth of shoppers actively browse the aisle for a given category, so marketers must leverage other ways to reach these shoppers perhaps in other areas of the store or via displays. While promotions and merchandising can be pivotal in influencing some purchases, these efforts will have a limited impact on others. Well-crafted marketing efforts at different points along the shopper path to purchase can result in both cost savings and more effective shopper marketing programs.