Bank Customers embrace Digital, but still Seek Omnichannel Options.

September 5, 2013

![]() Digital banking—customer interactions and transactions that take place via web, mobile and other digital channels—is no longer just a complementary element of retail banking services in the US, according to a new eMarketer report, “Digital Banking Trends: With Consumer Preferences in Flux, Is Omnichannel the Answer?”

Digital banking—customer interactions and transactions that take place via web, mobile and other digital channels—is no longer just a complementary element of retail banking services in the US, according to a new eMarketer report, “Digital Banking Trends: With Consumer Preferences in Flux, Is Omnichannel the Answer?”

For more than a decade, banks have used digital touchpoints to provide more convenience to customers, and, in turn, wring operational costs out from common transactions like bill payments and account transfers. However, many customers still show a strong preference for having convenient access to a physical banking center, especially when seeking out financial advice or performing more complex, emotionally involved transactions.

An omnichannel approach—serving and engaging with customers in an “anytime, anywhere” fashion—is being touted as a way to give banks of all types and sizes more flexibility to meet consumers’ constantly evolving preferences.

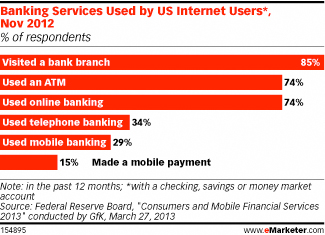

According to a November 2012 study from the Federal Reserve Board, branches and ATMs—a physical banking footprint—are still widely used by consumers. Eighty-five percent reported visiting a bank branch in the past 12 months, the most out of any category. Nevertheless, just as many respondents used online banking as they did an ATM—74%—underscoring the importance of digital channels to banks and their customers.

Online banking is commonly used across the spectrum of consumer segments, although the types of activities performed and frequency of usage vary when looking at different demographics.

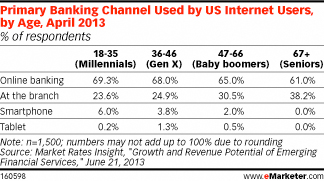

April 2013 research from Market Rates Insight found that more than three out of five internet-using millennials and seniors alike cited online banking as their primary channel. In addition, 6% of millennials reported using a smartphone as their primary banking channel—a stark contrast compared to seniors, none of whom used mobile devices as a primary banking touchpoint.

However, according to a May 2013 study released by the Gallup Business Journal on consumer interaction with banks, going to a branch was still the preferred channel for opening or closing an account, applying for a loan, seeking financial advice, reporting a problem or annoyance, inquiring about a fee and making deposits.

Numerous challenges in adopting an omnichannel strategy persist, though. A June 2013 Winterberry/IAB study found that factors such as the lack of appropriate tools or technologies, and internal operational challenges were key inhibitors preventing US marketing professionals in general from implementing an omnichannel approach.

Serving customers on their own terms requires a mix of organizational alignment, technological prowess and operational effectiveness—all areas that banks need to address to achieve omnichannel nirvana.

Courtesy of eMarketer