An update on US consumer sentiment: Consumers see a brighter future ahead

March 2, 2024

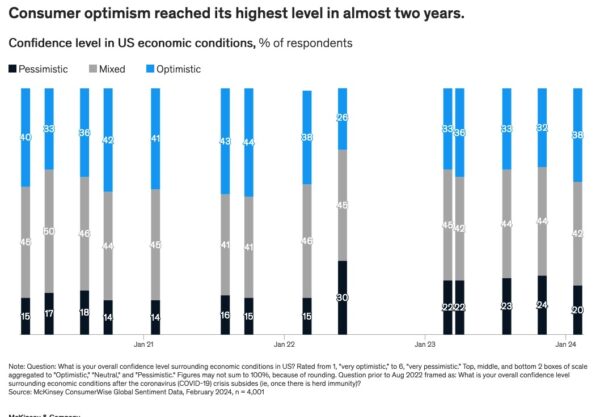

In February, concerns about inflation decreased slightly from the previous quarter, which helped consumer optimism about the US economy reach its highest level in almost two years. Although US consumers felt less pressure to save for an eventual rainy day, 20 percent were still pessimistic about the economy—but this represented the lowest reported pessimism rate since June of 2022 (although consumers were still more pessimistic than they were at the beginning of the COVID-19 pandemic). The following five charts highlight the findings from our latest ConsumerWise research in the United States.

My confidence has gone up when it comes to the state of the economy. There’s been a lot of positive change overall as the stock market has gone up, my personal portfolio has gone up, and we’ve seen more positive talk about the economy. Even spend at my local store seems to be higher.

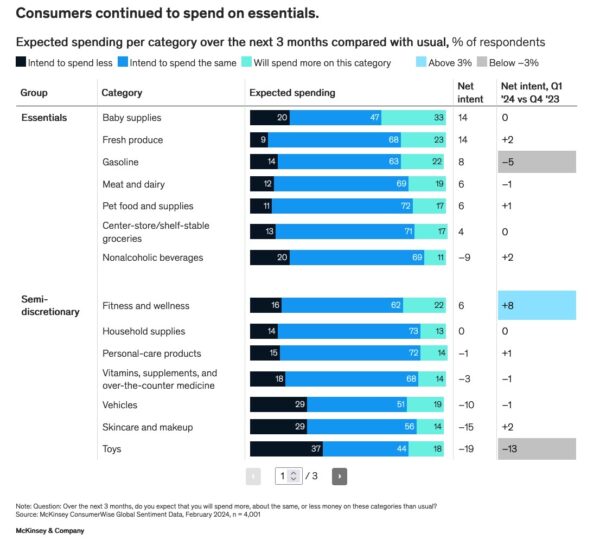

Consumers indicated they plan to increase their purchases of essential items. The average consumer said they expected to spend more on fresh produce, meat and dairy, and center-store categories (which include the items one might expect to find in the center of a grocery store, such as shelf-stable foods or frozen foods). Among discretionary items, consumers expressed in February a higher intention to spend on travel and home (such as on short-term rentals, home improvement, hotel resort stays, and flights) than they did in the fourth quarter of 2023.

Consumers anticipated reducing their purchases of toys compared with last quarter—no surprise, given that toy sales are typically higher during the holiday season than at the beginning of a new year. Meanwhile, consumers said they expect to allocate more of their budget toward fitness and wellness, once again, in line with typical spending habits at the beginning of a new year.

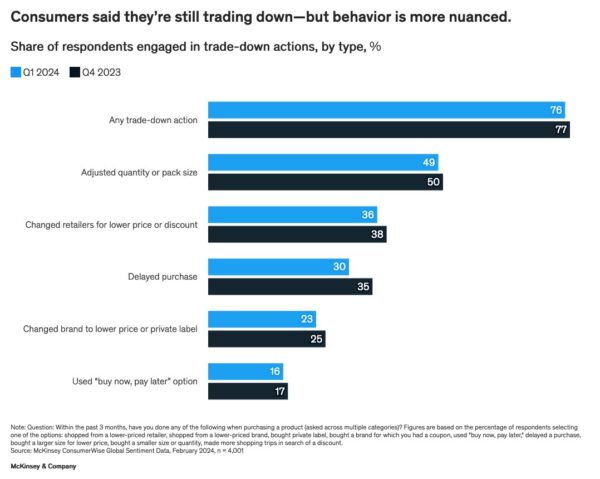

Trading down—or changing the type or quantity of purchases for better pricing and value—was still prevalent among consumers in February, although slightly fewer consumers reported trading down this month compared with the end of 2023. Younger consumers traded down more than older consumers, and, not surprisingly, low- and middle-income consumers traded down more than high-income consumers. Among lower-income consumers, there was a split among generational lines: millennials and baby boomers in this group reported trading down less frequently in February compared with the last quarter of 2023, while Gen Z and Gen X consumers in this group reported trading down more frequently.

Fewer consumers reported switching to lower-priced retailers and brands in February compared with the end of last year. The reported use of “buy now, pay later” services plateaued in February, and fewer consumers said they delayed a purchase in the past three months.

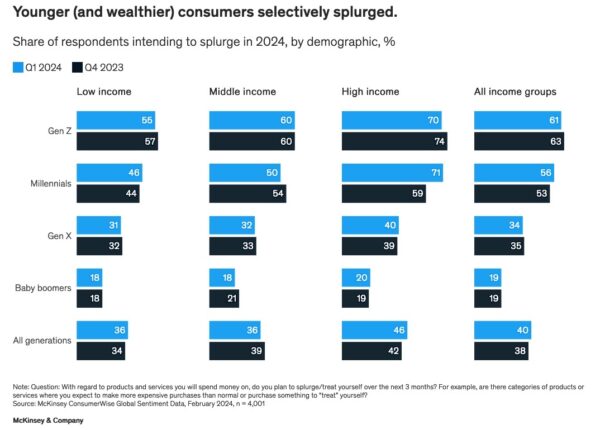

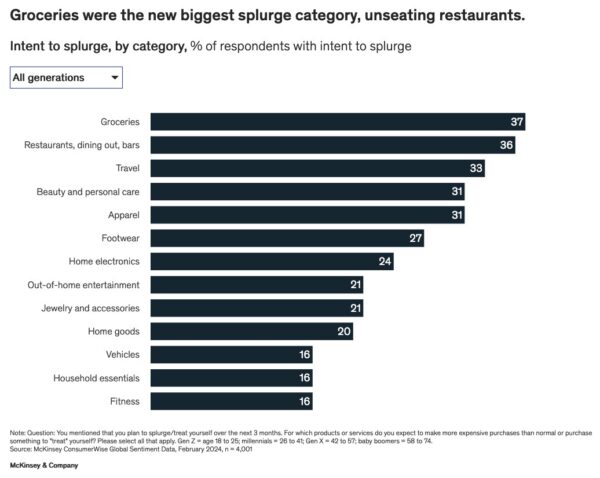

Consumers expressed a desire to splurge, and more than a third of respondents in our survey said they expected to splurge on food. But consumers’ ideas about what to splurge on have evolved: rather than splurging on dining out, consumers said they intended to splurge on food at home more than they did at the end of 2023. This change was most evident among Gen Zers and millennials.

Travel also became a more popular splurge category in February, moving ahead of apparel and beauty, which it trailed in the last quarter of 2023. More baby boomers said they planned to splurge on travel in the next three months than any other age group.

As inflation figures continue to fluctuate, will consumers continue to gain confidence in the economy and, therefore, continue to express an interest in splurging? Or will higher-for-longer interest rates slow spending? Watch this space for regular updates on the state of the US consumer. Check out our ConsumerWise page, and contact us for data from previous updates or additional insights.

ABOUT THE AUTHOR(S)

Christina Adams is a partner in McKinsey’s Dallas office, Kari Alldredge is a partner in the Minneapolis office, Lily Highman is a consultant in the New York office, and Sajal Kohli is a senior partner in the Chicago office.

The authors wish to thank Isabelle Engelsted, Alex Lequerica, Andrew Pitakos, Tom Skiles, and Eitan Urkowitz for their contributions to this article.