Signs of Optimism – or at least, Acceptance – in American Spending Trends

January 23, 2014

As 2014 approaches the end of its first month, many Americans are still sorting out their financial plans for the near future. With the government actually open for business – an improvement over last October – it should be a foregone conclusion that Americans may be facing the future with a bit more spring in their spending plans than in September of 2013, when the much-discussed federal shutdown was looming. But what about year over year? Are Americans loosening their purse strings or doubling down on pinching pennies?

As 2014 approaches the end of its first month, many Americans are still sorting out their financial plans for the near future. With the government actually open for business – an improvement over last October – it should be a foregone conclusion that Americans may be facing the future with a bit more spring in their spending plans than in September of 2013, when the much-discussed federal shutdown was looming. But what about year over year? Are Americans loosening their purse strings or doubling down on pinching pennies?

Big ticket attitudes bounce back

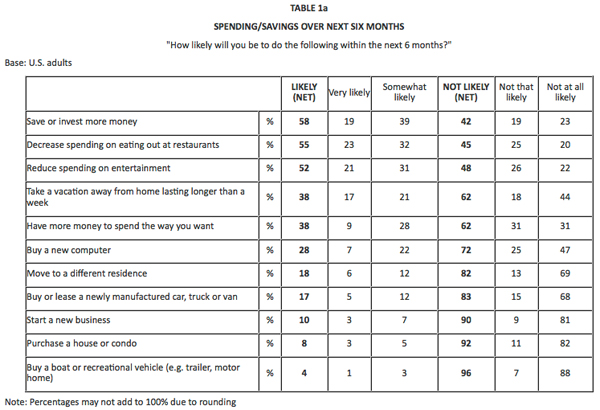

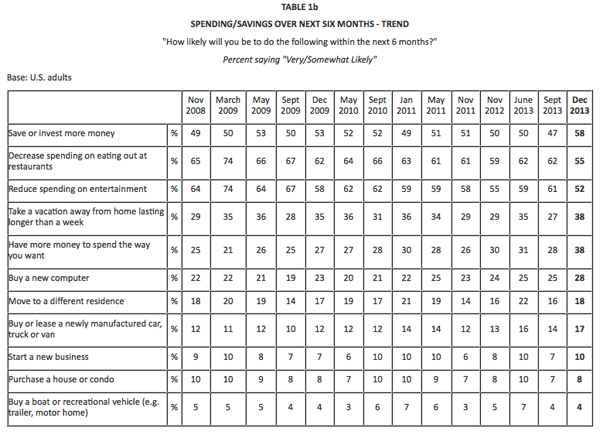

Americans are less likely than in September to say that they plan on decreasing their spending on eating out at restaurants (55%, down 7 points) and reducing spending on entertainment (52%, down 9 points) within the next six months.

On the other hand, U.S. adults are more likely to say they will save or invest more money within the next six months (58%), when compared to both last September (up 11 points) and the previous November (up 8 points). Americans are also more likely to say that they will take a vacation away from home lasting longer than a week (38%, up 11 points from Sept. 2013 and 9 points from Nov. 2012) and that they will have more money to spend the way they want (38%, up 10 and 8 points, respectively).

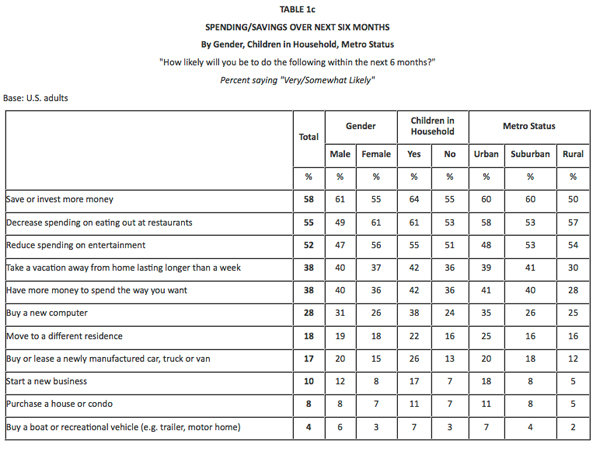

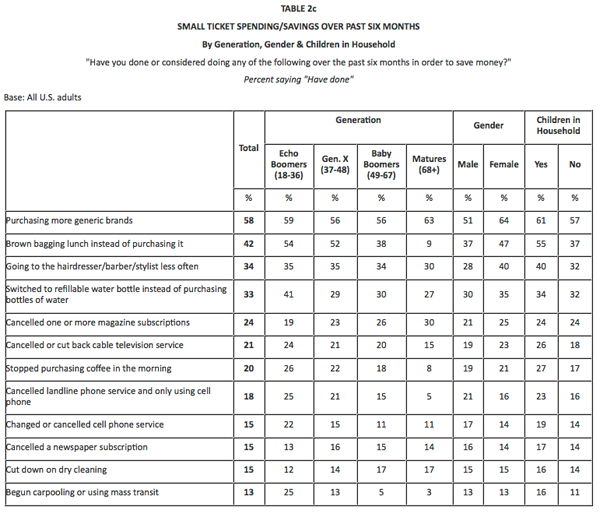

Rural Americans seem less optimistic than their urban and suburban counterparts: they are less likely to say they anticipate saving or investing more money (50% rural vs. 60% urban and 60% suburban), taking a vacation away from home lasting longer than a week (30% vs. 39% and 41%, respectively), and having more money to spend the way they want (28% vs. 41% and 40%, respectively).

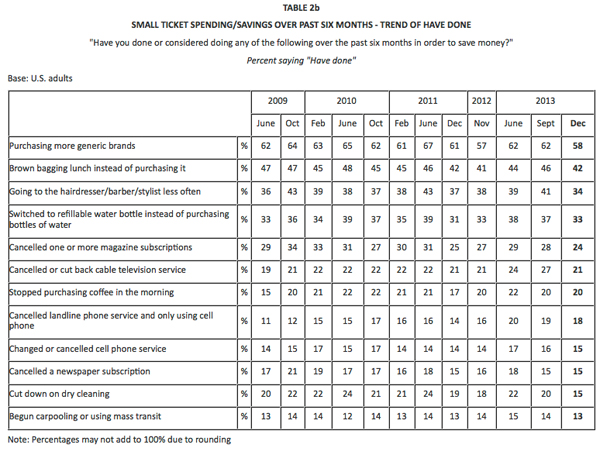

Small ticket spending plans also on the rise

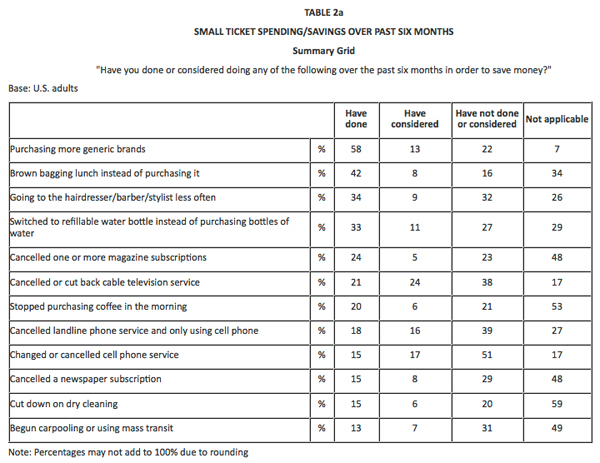

There are signs of growth in small ticket expenditures as well, with modest year over year drops in going to the hairdresser/barber/stylist less often (34%, down 4 points from Nov. 2012), canceling one or more magazine subscriptions (24%, down 3 points) and cutting down on dry cleaning (15%, down 3 points) over the past six months.

More prevalent are changes vs. last September, with results again indicating Americans are making fewer spending sacrifices:

- Going to the hairdresser/barber/stylist less often (34%, down 7 points)

- Cancelled or cut back cable television (21%, down 6 points)

- Cut down on dry cleaning (15%, down 5 points)

- Purchasing more generic brands (58%, down 4 points)

- Brown bagging lunch instead of purchasing it (42%, down 4 points)

- Switched to refillable water bottle instead of purchasing bottles of water (33%, down 4 points)

- Cancelled one or more magazine subscriptions (24%, down 4 points)

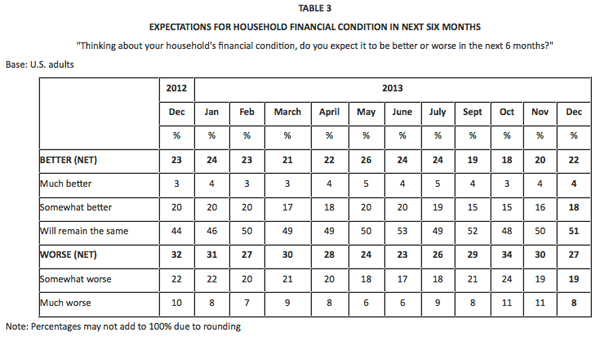

Is “not getting worse” good enough?

It’s tempting to look at these small and big ticket indicators as signs that American attitudes toward the economy are improving – and this is true, up to a point. Over two in ten Americans (22%) expect their household’s financial condition to improve in the next six months; this is comparable to a year prior (23%).

However, more notable is a trend away from the expectation that Americans’ household financial conditions will get worse, which at 27% is down 5 points from a year ago. Expectation that it will remain the same, at 51%, is up 7 points.

These attitudinal shifts, coupled with recent and planned spending trends, may be indicating that Americans feel they have cut back enough, and that if things aren’t going to get better for them any time soon, then they’ll at least settle for things not getting any worse.