The economic state of Latinos in America: Advancing financial growth

December 14, 2023

Financial services and the tools they provide can be invaluable for economic mobility and wealth building, but many of the benefits have been hard to reach for Latinos, many of whom live with unmet needs. While they represent about 20 percent of the US population and are a growing economic bloc, Latinos have not had access to many of the benefits of financial services. These challenges contribute to persistent inequalities. For example, the median White household has five times the wealth of the median Latino household.

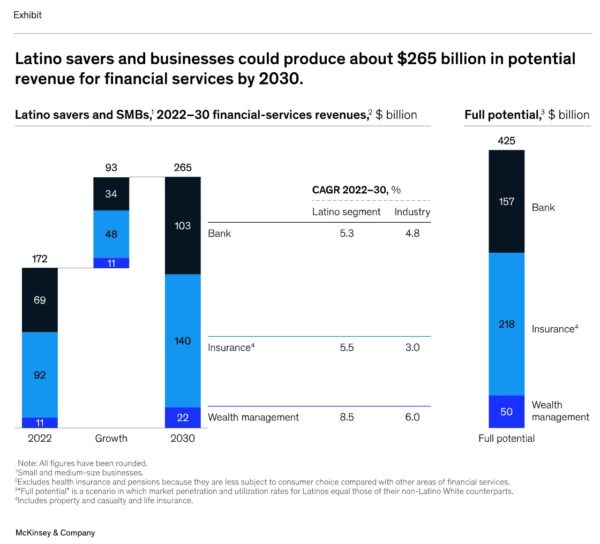

Serving Latino customers more effectively can create a market-beating virtuous cycle of granular growth, profit, and environmental, social, and governance priorities. Our analysis shows that revenue from Latino households (whom we will refer to as savers) and from small and medium-size businesses (SMBs)—those with revenues of $30 million or less—is already around $170 billion. We project that the market will organically grow to about $265 billion in 2030 (exhibit), 8 percent of the total value of the financial-services market.

Some forward-looking industry participants are already making progress and improving offerings for Latino customers. But for the industry as a whole, slow action or complacency would be risky. In our new report, The economic state of Latinos in America: Advancing financial growth, we highlight the social and economic benefits of serving Latino savers and SMB owners6; identify internal organizational barriers and consider methods to help build strong, productive relationships with Latino savers and business owners; and discuss how institutions can zero in on the right strategy for serving Latino customers, give an overview of three strategic approaches, and outline the role of venture capital (VC) and private equity (PE) investors in growing the segment’s economic mobility. While this report focuses on Latino savers and business owners, many of the strategies we recommend can also help financial institutions strengthen their relationships with other often-overlooked customer groups.

Latino savers can power $240 billion in financial services revenue, but barriers remain

Our analysis suggests that revenue from Latino customers in banking, insurance, and wealth management will increase by more than 50 percent, from about $155 billion in 2022 to about $240 billion in 2030. McKinsey research finds that compared to the general population, Latino savers are more loyal to institutions they already work with when they want to find new solutions such as investment services.

Although some institutions are making headway on meeting these needs, barriers between institutions and Latino consumers remain. These barriers include difficulty accessing bank branches, low levels of trust, and systemic features that make it difficult to accurately assess many Latino savers’ creditworthiness.

These barriers have helped perpetuate pain points for Latino savers. Indeed, 55 percent of Latino savers in our research described themselves as dissatisfied with the financial services sector. Hurdles include a lack of Spanish-language services and an unmet need for affordable and efficient international money transfers, which are especially important because Latinos’ savings tend to be 11 percent lower than that of their non-Latino White peers. Of course, financial products can help savers build wealth, but Latino savers are the least likely to participate in the equities market and lag behind the general US population in having life-insurance coverage.

Better serving Latino business owners could produce $25 billion per year in revenue

Latinos are a highly entrepreneurial group, starting businesses at three times the rate of the general population. Our analysis also suggests that Latino business owners’ spending on banking and insurance will grow from $17 billion in 2022 to $25 billion in 2030.

Latino business owners are distinguished by their focus on their businesses’ long-term growth and their higher-than-average willingness to pay for relationship management services. Financial institutions can meet these preferences by providing comprehensive solutions, particularly culturally competent relationship-oriented services such as financial planning.

Some financial institutions, such as community development financial institutions (CDFIs), aim to offer Latino business owners what they need. However, one persistent obstacle for Latino business owners is difficulty obtaining funding. Our analysis revealed a $200 billion lending gap between Latino-owned SMBs and their White-owned counterparts. This gap is maintained by long, daunting lending processes—for a group that already struggles to trust financial institutions. And though some institutions, such as CDFIs, are working to support Latino business owners, their relatively small size makes their offerings hard to scale.

Aligning strategies with commercial goals

Developing effective approaches to serving Latino consumers effectively is a significant undertaking. We outline three steps institutions could take to identify the right strategy for approaching Latino customers, discuss three major strategies, and spotlight the role private-market investors can play in this ecosystem.

Three steps to get to the right strategy

Institutions could follow three steps to identify the right strategic approach for serving Latino customers.

The first step is to identify key customer segments and create a strategic approach that fits. On the figurative day one of the effort, institutions could start with understanding their current Latino customers’ characteristics, product usage patterns, and needs.

The next step is to develop compelling value propositions and commercial strategies that resonate with key customers. As a starting point, institutions could identify products that best cater to Latinos customers’ needs and that reach them in the most effective channels. Institutions could then use those insights to develop holistic offerings, testing and refining them to ensure they meet customers’ requirements. As part of this step, decision makers would also articulate the specifics of their commercial initiatives, such as go-to-market strategies and products for this audience.

Finally, financial institutions would focus on integrating the chosen approach into their overall strategy and commitments.13 Day-one actions include reviewing existing capabilities and resources to identify areas of overlaps in serving Latino customers. Scaling requires identifying the elements—enablers—that are critical to the success of their strategies.

Three strategic approaches

Depending on their goals and philosophies, financial institutions could use three strategic approaches to meet Latino customers’ needs.

The first approach focuses on commercial value, in which institutions work to rapidly acquire and grow revenue from key customers by fulfilling their specific needs and pain points. For instance, US institutions could use partnerships with major banks in Latin America to give highly profitable Latino customers a continuous experience.

The second approach focuses on inclusion, which requires a long-term view. Institutions emphasizing inclusion might offer basic financial services and products to savers who live in banking deserts, and who have little or no credit visibility or English proficiency. Fee structures and products might be designed with an emphasis on supporting savers’ everyday finances.

The third approach focuses on inclusive growth, which aims to better address the needs of customers who already have a relationship with financial institutions. Institutions could work on measures such as partnering with CDFIs to support business owners from historically overlooked communities in building their credit profiles and accessing credit.

Private investors’ role in financial inclusion

Private-market institutional investors—specifically VC and PE firms—could play a central role in boosting economic mobility for Latino savers, business owners, investors, and investing professionals. Most obviously, firms could consider investing in Latino-owned SMBs.

Having more capital under Latino management and increasing Latino representation among investing professionals could help investors produce more value.14 Of the $11.7 trillion in assets under management in the private markets,15 less than 1 percent are directly managed by Latino-controlled entities.16 And at 4 percent, Latinos are also underrepresented in the ranks of investment professionals.

Finally, institutional investors could help bolster themes that support Latinos’ economic mobility and boost financial service uptake among Latino customers. One area to consider is homeownership, a common engine for household wealth building.

Opportunities to offer Latino customers more tailored solutions are plentiful. Success will go to the early movers.

About the author(s)

Alberto Chaia is a senior partner in McKinsey’s Miami office; Arsenio Martinez is a partner in the Washington, DC, office, where Nick Noel is an associate partner; Marukel Nunez Maxwell is a senior partner in the New York office; and Lucy Pérez is a senior partner in the Boston office.

The authors wish to thank Maya Aidlin-Perlman, Clara Carvalho, Roukaya El Houda, Jose Miguel Errazuriz, Kayla Getter, Juliette Low Fleury, Monica Rex, Alexia Sabogal, Gil Sander Joseph, Kelly Song, Laura Tamayo Castillo, Tre Tennyson, and Benjamin Topa for their contributions to this report.