US holiday shopping 2023: Consumer caution and retailer resilience

November 7, 2023

By Colleen Baum, Tamara Charm, and Kelsey Robinson

The final stretch of an increasingly long holiday shopping season is critical for retailers, particularly as consumers focus on value and new shopping journeys.

After a year of modest sales growth, retailers face a critical holiday sales season. The big question on everyone’s mind: Will consumers—whose spending habits have challenged efforts at curbing inflation—finally pull back?

Although shoppers are feeling better than they were this time last year, general consumer sentiment about the US economy is one of uncertainty. That means there are no guaranteed wins for retailers as consumers decide how much to spend through the remainder of the holiday shopping season, which can represent up to 40 percent of sales for discretionary retailers.

Some consumers will trade down, while others will splurge. Whatever their holiday shopping strategy, retailers are finding ways to connect with their customers. Some businesses emphasize membership and loyalty programs, which come with discounts and early access to deals. Price match guarantees and widened return windows—of up to four months in some cases—are other strategies retailers are implementing. These purchase incentives, however, are only one part of the equation: retailers, if they haven’t already, should also invest in an improved supply chain and omnichannel experience to provide greater convenience to shoppers.

Retailers have put many of these strategies to work in past years, but in a challenging environment with high stakes, will they be enough to meet consumer expectations while also proactively managing store costs and fulfillment expenses?

This article presents findings from McKinsey’s ConsumerWise team and our latest Consumer Pulse Survey, which outline when consumers will shop for the holidays, how much they will spend, and what matters most to them during this time. We also recommend four actions that retailers could consider to win consumer spend through the holidays.

The survey was in the field from October 17 to October 19, 2023, and collected responses from more than 1,000 consumers in the United States (sampled and weighted to match the general US population, ages 18 to 74). These insights build on the work we have undertaken since March 2020, when we began to regularly conduct consumer surveys and combine our research and analysis with third-party data on US spending to glean insights into how consumer sentiment has shifted since the beginning of the COVID-19 pandemic.

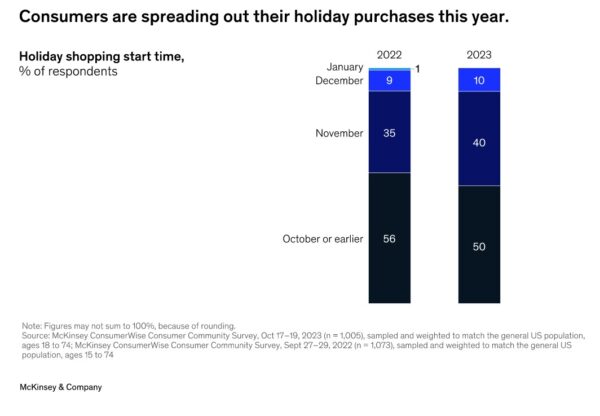

Holiday head start. This year’s holiday shopping season started earlier and will last longer than it did in 2022. As early as September, retailers started promoting holiday ads on social media, with many more following in October. The race to launch ever earlier holiday promotions has created one long, continuous year-end promotional cycle, in hopes of capturing consumers who may be trying to spread their purchases out over a longer period.

While most consumers started their holiday shopping in October or earlier, 40 percent of consumers this year say they intend to start holiday shopping in November, compared with 35 percent in 2022. Additionally, of the consumers who started their holiday shopping in mid-October, only about a quarter of them completed more than half of their holiday shopping, leaving plenty of room for retailers to reach these shoppers through the end of the year. November and December, therefore, are still critical holiday shopping months.

Consumers say they are shopping earlier and that their holiday shopping will last longer this year, in both cases citing price as their primary motivation for doing so. Shoppers who started browsing for products earlier did so in anticipation of price increases; other shoppers, expecting sales to come closer to the holidays, may have delayed their purchases. In addition to concerns about availability and lead times, consumers say they want to make their purchases over a couple of months rather than all at once.

Consumers are trading down. Seventy-nine percent of consumers say they are changing their shopping behaviors to trade down (swap their purchases for cheaper alternatives or forgo purchases altogether)—an increase of five percentage points compared with July 2022. This can be observed across generations and income levels, although younger shoppers are more likely to trade down (despite ranking better prices and promotions as slightly less important than other factors). In general, this means that value and promotions will be increasingly important to retailers.

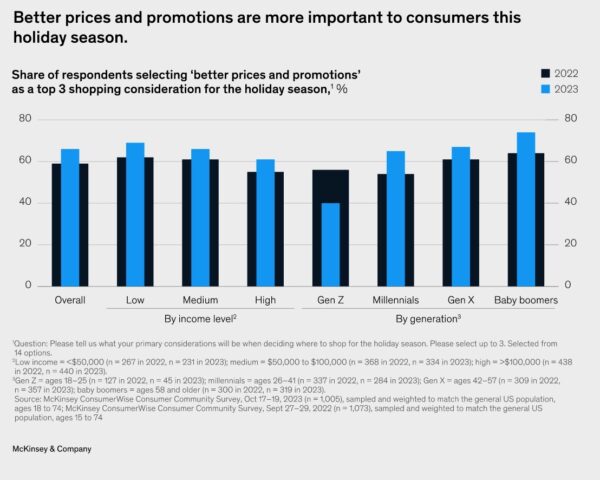

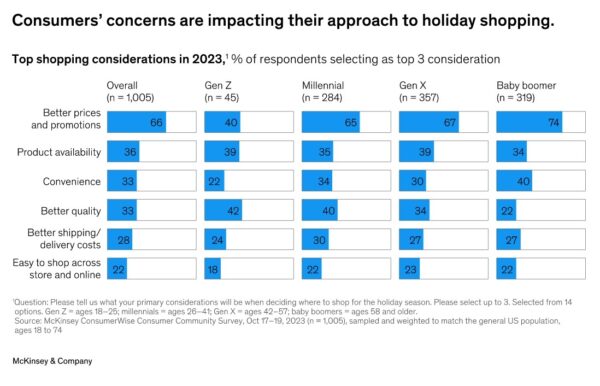

Price, promotions, priorities. Although the rate of inflation in the United States has slowed from its mid-2022 peak, other issues—such as uncertainty over the economy and geopolitical issues—have occupied consumers’ minds. Given these circumstances, most consumers rank better prices and promotions as their top consideration for holiday shopping this year (66 percent), higher than how they ranked this consideration last year (59 percent), and significantly above their next highest considerations, which are product availability and convenience.

While Gen Z cares about prices, their considerations are more evenly distributed than those of other generations, and they actually rank quality as slightly more important than prices. Gen Zers also express the least concern of any generation with respect to convenience.

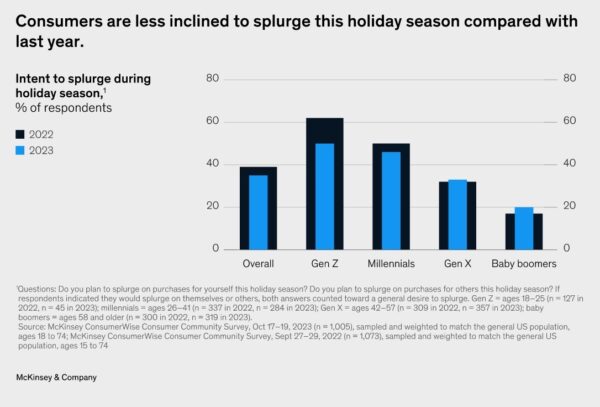

Splurging falls out of favor. Most Americans don’t intend to splurge on gifts this year (except for a group of “enthusiasts” with plans to spend big): the percentage of consumers who intend to splurge on either themselves or others this holiday season declined four percentage points year over year, from 39 percent in 2022 to 35 percent in 2023.

This decline is mostly fueled by Gen Z belt-tightening: in this cohort, there was a 12-percentage-point decrease in consumers who intend to splurge—although they intend to splurge at a higher rate than other generations. Despite Gen Z’s practical approach to holiday shopping this year, they still indicate that they are more excited to shop this year compared with last year, and that they expect to spend more on gifts for others and themselves than they did last year. Meanwhile, Gen Xers and boomers actually express a greater intent to splurge.

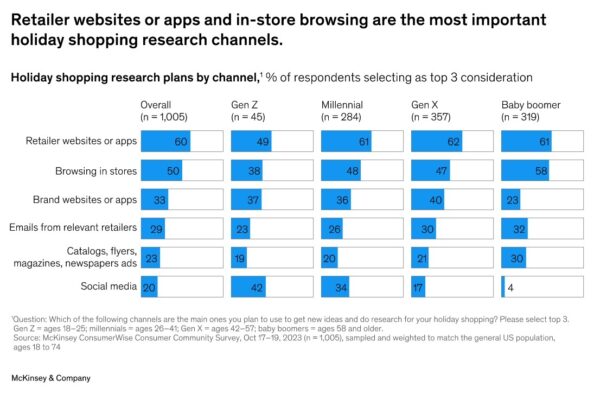

Bifurcated browsing. Consumers plan to do most of their holiday shopping research using retailer websites or apps and by browsing in-store, underscoring the importance of a strong omnichannel experience. Social media is an important discovery channel, too, but mostly for Gen Z and millennials.

Just over a quarter of consumers indicate that they plan to shop online more this season compared with last year, while fewer consumers plan to shop in-store. Despite the ongoing shift toward online shopping, the physical-store experience still matters: 85 percent of consumers expect to purchase at least one item in-store, while 12 percent plan to pick up purchases in-store.

Retailer websites or apps and in-store browsing are the most important holiday shopping research channels.

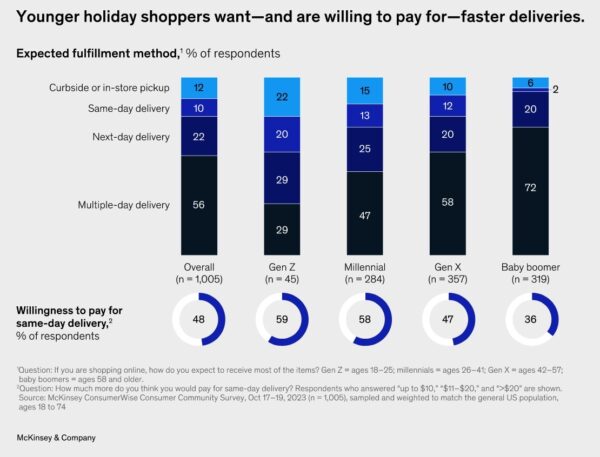

Next-day needs. Younger shoppers expect their products to be delivered or available for pickup much sooner than older shoppers—and are more willing to pay for expedited delivery. About half of Gen Z consumers say they expect to use same-day or next-day delivery, and over 50 percent say they will pay for same-day delivery. Gen Zers are much more averse to deliveries that occur over multiple days than Gen Xers and boomers are, and more of them are willing to pick up their purchases either curbside or in-store.

Shoppers who choose a next-day delivery option expect their items to be delivered on time with a damage-free guarantee from the retailer. Meanwhile, consumers who are willing to travel to a store for curbside or in-store pickup expect to enjoy promotions or earn loyalty program points for their efforts.

Plan to pay. Consumers prefer to use credit cards to pay for their holiday purchases more than any other payment method, followed by debit card or cash. Once again, Gen Z shoppers are demonstrating preferences that differ from those of older generations: buy now, pay later platforms are most popular among this group—at more than two times the rate of the average consumer—although Gen Zers are accruing credit card debt faster than other generations. Gen Z also indicates more interest in retailer-provided installment plans than other generations.

In response to this year’s holiday shopping trends, we recommend that retailers consider the following actions. These actions extend across the end-to-end value chain and can help retailers get products to consumers in a quick, seamless, and cost-effective way.

- Inspire beyond promotions. As consumers grapple with whether to splurge or save this year, retailers have an opportunity to inspire their customers through storytelling. Focusing on the experiences that come with a purchase—such as crafting for the holidays, setting a beautiful table for family gatherings, or indulging in self-care—may motivate purchases more effectively than relying solely on discounts. To achieve this, retailers should tailor their communications by channel. For example, video content on social media that highlights the benefits of a product may resonate most deeply with consumers who are comparison shopping.

- See demand generation through the “ninth inning.” As shopping journeys are becoming increasingly omnichannel, retailers should meet customers where they are to capture them throughout the holiday shopping season. Retailers are using new technologies, such as AI, and communities, such as store employees and micro-influencers, to deploy curated and personalized content online and at scale. In-store experiences can be bolstered by digital enhancements, such as augmented-reality apps and cashierless shopping. Meanwhile, live stream shopping is also gaining traction, especially with younger consumers.

- Personalize promotions for consumers. Leading retailers focus on targeted pricing and personalized offers to deepen customer loyalty, based on a comprehensive view of individual customers. This requires having a baseline understanding of when and what consumers buy and their sensitivity to price and promotions. As the holiday shopping window extends over a longer time period this season, a focus on driving customer loyalty is key. Targeted and personalized offers may also enable retailers to drive inventory sell-through while capturing incremental sales and profit.

- Continue to optimize the supply chain through January. Leading retailers will take a holistic view of their supply chains as they operate through the remainder of the holiday season, balancing both cost and service level. Online fulfillment, which includes last-mile-delivery cost optimization and buy online, pick up in-store promotions, will be a major focus area. Even with a focus on online fulfillment, retailers should consider holistic impact. For example, can the holiday promotion calendar be synched with parcel carrier volume commitments to ensure service at the lowest possible costs? Can more orders be fulfilled from stores to move through inventory with the greatest markdown risk? Finally, consumers remain concerned about product availability and shipping times, so we expect winning retailers to build trust by providing transparent communication about shipping dates and executing deliveries reliably through December.

About the author(s)

Colleen Baum is a partner in McKinsey’s New York office; and Tamara Charm is a partner in the Boston office, where Kelsey Robinson is a senior partner.

The authors wish to thank Kari Alldredge, Resil Das, Miranda David, Prabh Gill, Suahn Hur, Aniket Joglekar, Krishnanand M, Meaghan Shimota, Tom Skiles, and Natsuko Yamazaki for their contributions to this article.